Tender Prices – Coronavirus impacts & Brexit is back!

In these difficult and challenging times one of the biggest questions is what is the likely impact of the COVID-19 on the outlook for contractors and the impact on tender prices?

Our specialist cost consultant Rob Kennedy has brought the following information hot off the press from the Royal Institution of Chartered Surveyor’s Building Cost Information Service (BCIS).

Remember the subject of Brexit, which prior to COVID-19 consumed every hour of news and every column of newspapers? We know it never went away and the BCIS have kept a weather eye on the subject and comment on that to.

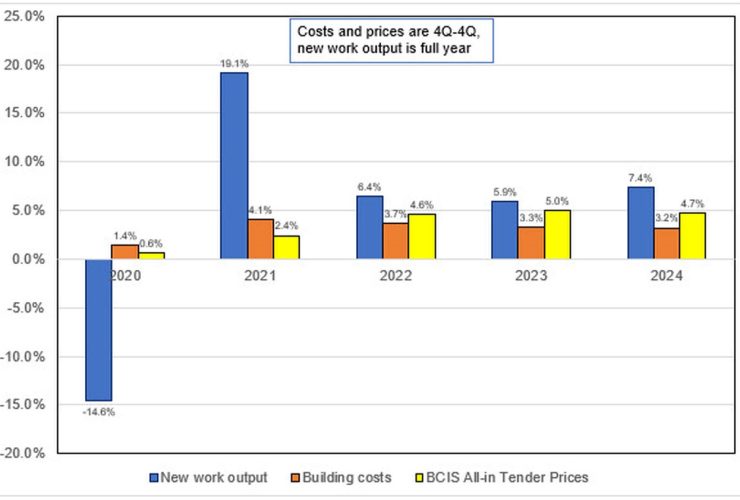

Helpfully the BCIS produced the following graphic which pretty much encapsulates all you need to know about their thinking on output costs and tender prices:

This ties in with our own experience and the comments made to ARK by contractors and clients. Tendering opportunities reduced whist clients interpreted the effects of COVID-19. There has been a wariness amongst clients of taking tenders to a market which may not be able to respond due to furloughing at main and sub-contractor level. But with a general return to construction at the end of May we are anticipating a greater willingness by all parties to engage.

BCIS state that tender prices will “Remain virtually unchanged for the rest of 2020 and rise slightly in 2021”. We think this reflects two conflicting pressures for contractors – uncertainty regarding consistent supplies of product and labour and potential price volatility v limited opportunities which traditionally keep pencils sharp – We have a sense that prices will have to increase, if for no other reason than the additional time it will take to build out schemes and the increased cost of prelims.

Looking forward BCIS are anticipating a Brexit impact stating “With the end of the Brexit transitional period in December 2020, continued uncertainty is expected, particularly in the private commercial sector, as it seems unlikely that any major agreements will have been made with the EU”. Once again, the uncertainty is likely to have a dampening effect with “tender prices are only expected to rise by 2.4% over the second year of the forecast” (2021/22)

However, over the whole period until 2024 BCIS estimate that “Output will rise by 23%, Costs will rise by 17% and Tender prices will rise by 19%”. If that is right striking deals early could be a sensible approach.

The ARK team of experienced project managers are available to help you at any stage in the development process from site finding to completing defects. Just contact Chris 07770532571 or email him at cseeley@arkconsultancy.co.uk to find out more.

Share

![]()

![]()

![]()

News & Insights

Read the latest housing sector news, blogs, and commentary from ARK.

Building Safety

By Luke Beard ·The deadline for registering an existing higher risk building (HRB) with the regulator and submitting the required key building information …

Are you ready for the Supported Housing (Regulatory Oversight) Act 2023?

By Nick Sedgwick ·If you are a supported housing provider, you need to be aware of the new regulations that are about to …

International Women’s Day 2024

By Chris Seeley ·The theme of International Women’s Day 2024 is the question ‘What does it mean to truly inspire inclusion?’, we asked our …

Subscribe to our newsletters for the latest industry insights

Our newsletters and reports will keep you updated on topical issues from the sector as well as what’s happening at ARK.